There is a question that reliably produces silence in executive meetings. How many projects are currently running in this organization?

Finance has one number, based on what has been funded. The PMO has another, based on what is formally registered. The functional heads have a third and considerably larger one, because they know what their people are actually working on. None is wrong. They describe different things, and the gap between them is where portfolio management is supposed to live.

Robert Cooper and his co-authors framed the underlying problem more sharply than most: there are two ways to succeed, and they are doing projects right and doing the right projects. Almost all management attention goes into the first. Portfolio management is the discipline concerned with the second, and it remains the weakest link in most organizations I work with.

What the portfolio is supposed to decide

Portfolio management is not project management at a larger scale. It operates on a different unit of decision: a project manager decides how work gets done, while a portfolio decides whether the work should exist at all and what it is allowed to consume while it does.

The most durable description of what a portfolio process is trying to achieve comes from Robert Cooper, Scott Edgett and Elko Kleinschmidt in Portfolio Management for New Products (2001). It is worth being precise about the origin: the book concerns new product development portfolios, not project portfolios in general. The framing proved general enough that project portfolio management literature adopted it, and these goals are now routinely cited as the goals of project portfolio management.

There are three, later extended with a fourth. Maximize the value of the portfolio. Achieve the right balance between project types, risk levels, and time horizons. Ensure the portfolio reflects the declared strategy. And keep total commitment within the resources actually available.

The fourth goal is the one that gets quietly abandoned. The first three can be discussed in a slide deck. The fourth requires someone to say no.

Antonio Nieto-Rodriguez makes a related point: strategy becomes real at the moment resources are committed to something specific. Until then it is intent. Portfolio decisions are therefore strategic decisions in the most literal sense, and delegating them to an administrative function guarantees that strategy stays on paper.

The classical cycle

The process is not complicated and has been documented for decades in broadly the same shape. PMI’s Standard for Portfolio Management describes it as performance domains rather than sequential steps, and notably treats capacity and capability management as a domain in its own right, alongside strategic management, governance, value, and risk. Stated as a cycle, it runs as follows.

- Intake. Requests enter through a defined channel, described in a consistent format.

- Evaluation. Each candidate is assessed against the same criteria: strategic contribution, expected benefit, cost, risk, and dependencies.

- Prioritization. Candidates are ranked — ordered against each other, not sorted into tiers where everything eventually becomes tier one.

- Capacity balancing. The ranked list meets reality. Available money, and more importantly available people, determine where the line is drawn.

- Authorization. Projects above the line start, with a named sponsor and a committed team. Projects below it do not, and are told so explicitly.

- Periodic review. The portfolio is reassessed on a fixed cadence and projects are continued, paused, or stopped on evidence rather than momentum.

- Benefits realization. Delivered projects are tracked beyond handover to establish whether the value used to justify them materialized.

None of this is controversial, and most organizations that struggle with portfolio management can describe the cycle accurately. The failure is almost never in the design of the process. It is in the condition of what enters it.

The gate that was never built

Prioritization is a comparison, and comparison requires that the things compared are described in comparable terms. This is where the cycle quietly collapses.

In practice, projects rarely enter a portfolio through evaluation. They enter through narrative. Someone senior mentioned it. It has a name that sounds strategic. It was on last year’s list and nobody removed it. By the time it reaches the portfolio review, the project is not a candidate to be assessed but a fact to be accommodated. The consequences are structural.

You cannot rank what is not defined. “Supply chain digitalization” and “reduce finished goods inventory by 20% in the EMEA network by Q3” are not comparable, and the vaguer one usually wins, because vagueness is hard to argue against.

You cannot balance capacity against undefined demand. Half-specified projects consume very real capacity — the same planners, the same data owners, the same three people who understand the ERP master data. The portfolio believes it has committed sixty percent of capacity while the organization is at a hundred and twenty.

You cannot stop what was never properly started. Cancellation requires an agreed reference point: this is what we said it would deliver, this is what it delivered. Without that baseline, stopping is a political argument, not a portfolio decision.

This is where the Strategic PMO usually finds itself. It is given accountability for portfolio governance, prioritization, and executive reporting, then handed inputs that cannot support any of it. It responds the way any function responds to bad inputs: more status collection, more consolidation, more slides. The organization concludes that the PMO is bureaucratic. The real problem is that it was asked to run a decision process on material that does not permit decisions.

Controlling the entrance

The most effective intervention I have made in portfolio environments has almost never been redesigning the process. It has been controlling what is allowed into it.

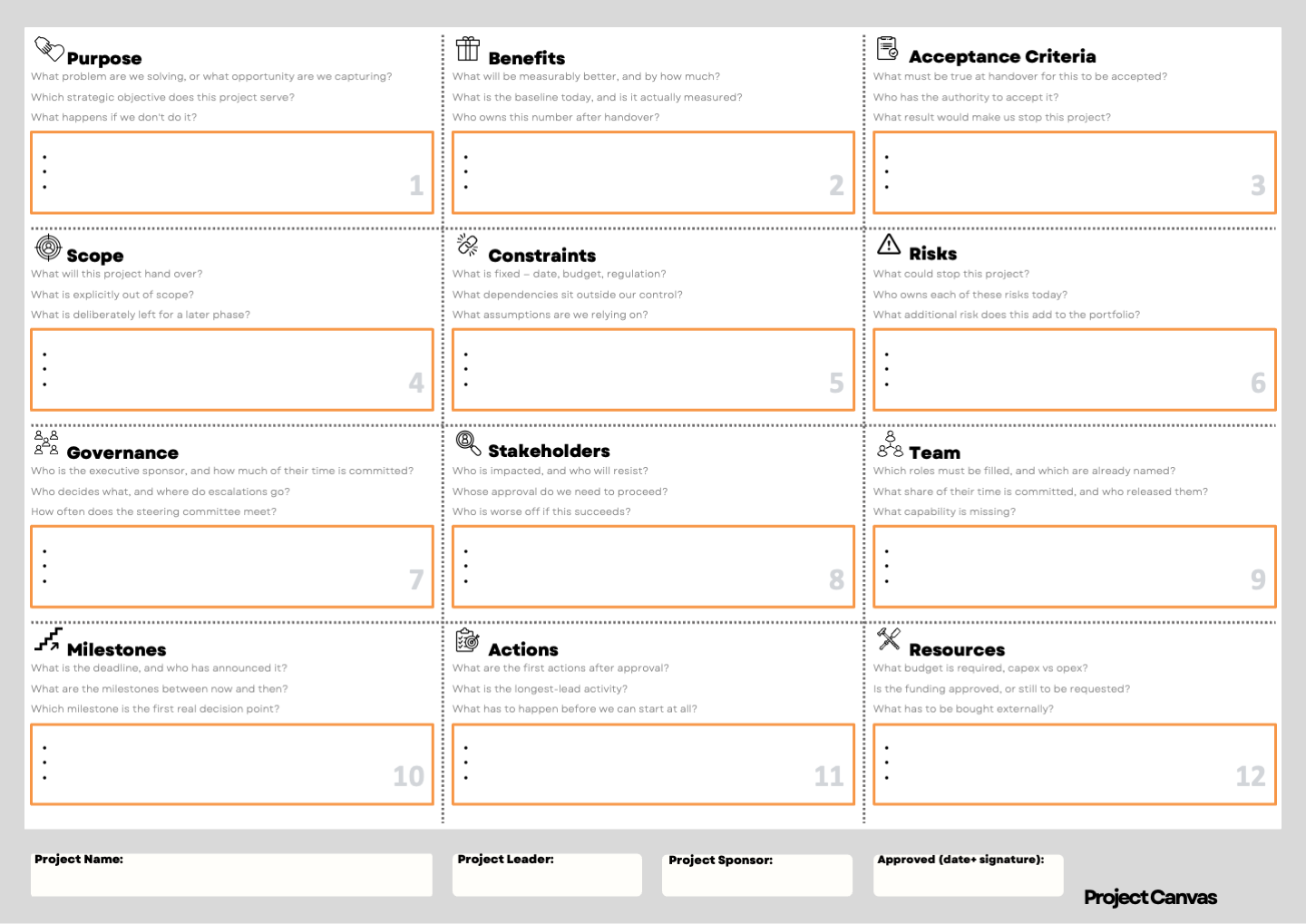

The instrument I use is an adapted Project Canvas, the one-page framework developed by Antonio Nieto-Rodriguez out of the same canvas thinking that produced the Business Model Canvas and, later, the Lean Canvas in startups. It covers four domains: why the project exists, who is accountable, what will be done and when, and the organizational context it lands in. In its original form the purpose is facilitative — a shared page for executives and teams to think on.

Over the years I have used it for something narrower. Not a conversation tool, but an admission criterion.

The intake version of the canvas: twelve fields, completed in the numbered order, three questions each.

The version I work with holds twelve fields completed in a fixed order rather than wherever the author feels most confident. Purpose, benefits, and acceptance criteria first. Scope, constraints, and risks next. Then governance, stakeholders, and team. Milestones, actions, and resources last, because effort and cost can only be estimated once the other nine fields exist.

Under each field sit three questions. This is the part that took years to get right. An empty field labelled “Benefits” invites ambition. A field asking what the baseline is today, whether it is actually measured, and who owns the number after handover invites information. Several questions are deliberately uncomfortable: what result would make us stop this project, who is worse off if it succeeds, whether the funding is approved or merely expected, and who released the named team members from their existing work.

Two elements at the bottom of the page are not optional: the executive sponsor is named next to the project leader, and the approval carries a date. A signature that cannot be compared to anything is not a baseline.

Used as a gate, the canvas separates two states organizations habitually blur. A project that is defined, funded, sponsored, and resourced enters the portfolio. One that is none of those things is not rejected as an idea, but neither is it admitted as a commitment. It goes back with a specific list of what is missing, and the portfolio’s capacity stays unspent until it returns.

What changes when the gate holds

The effects appear within one or two review cycles. Comparison becomes possible, because every candidate arrives in the same structure. The capacity conversation becomes concrete, because named people and committed time appear before approval rather than after the first missed milestone. Sponsorship becomes real, because asking in writing how much of the sponsor’s time is committed filters out initiatives nobody senior intends to support. And stopping becomes legitimate: when acceptance criteria and cancellation conditions were signed, ending a project executes an agreement instead of making an accusation.

None of this makes portfolio management easy. It makes it possible. A portfolio process is a decision system, and no decision system functions on inputs that do not permit decisions. Most organizations do not have a portfolio problem. They have an intake problem that surfaces, six months later, as a delivery problem.

The cheapest moment to fix an initiative is before it becomes one.